What is a Defective Return Under Section 139(9)?

If the Income Tax Department identifies any errors or omissions in the ITR then it will be treated as defective. When a return is termed as defective, the taxpayer receives a notice under Section 139(9) and within15-days we need to correct the errors.

The errors or omissions may include:

· missing information,

· discrepancies between reported income and TDS or

· incorrect deductions.

Common reasons for receiving a defective return notice include:

- Missing information: For instance, not mentioning salary as per Form 16 from all the employments during the relevant financial year.

- Mismatched Income Details: Differences between the income reported in your return and the income recorded in Form 26AS.

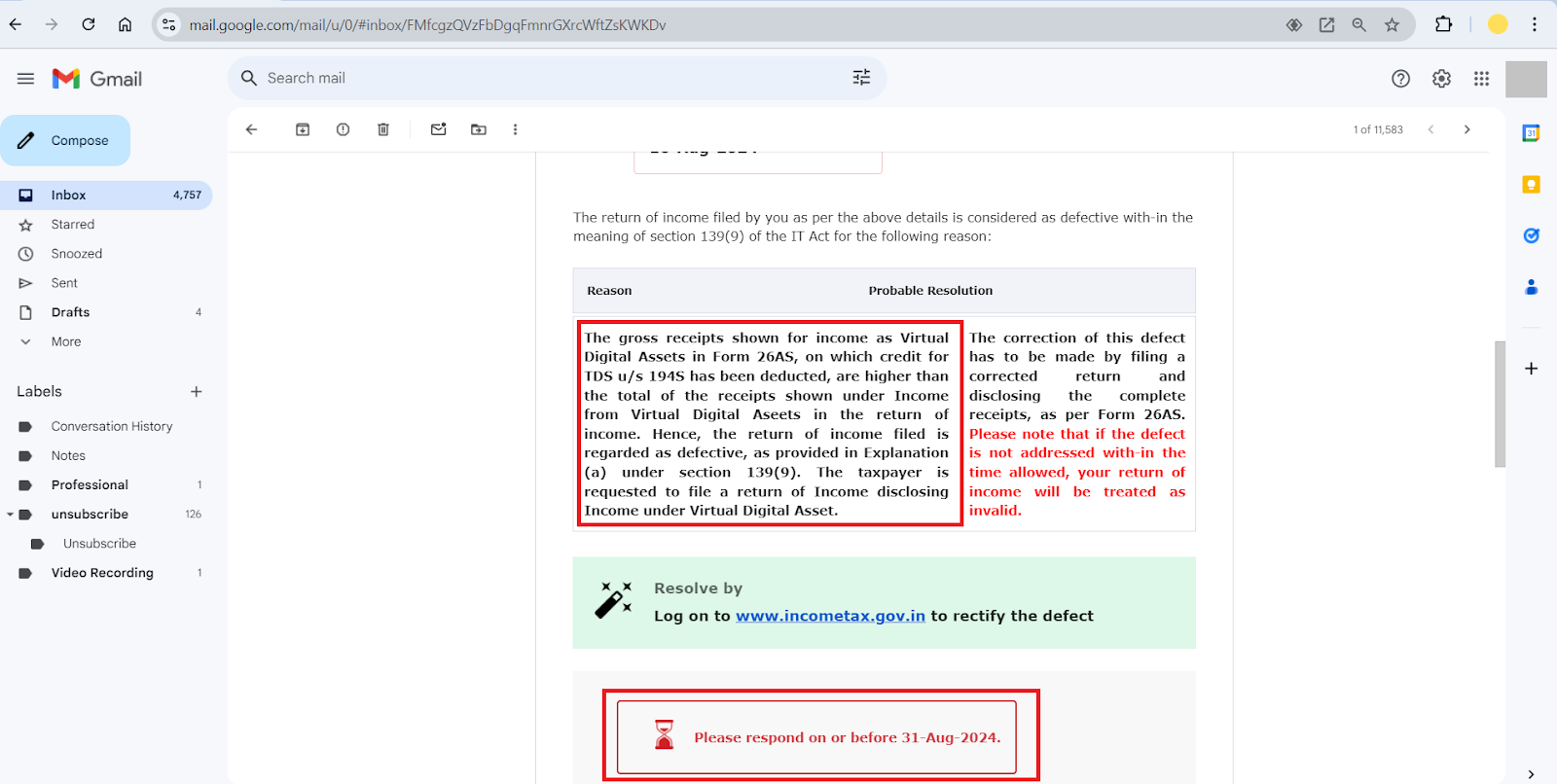

- Unreported Income: Omitting income from sources like interest, dividends, Virtual Digital Assets (VDA/ Cryptocurrency) or rental income.

- Incorrect Deductions: Claiming deductions that you’re not eligible for or incorrectly reporting deductions.

Step-by-Step Process to Rectify a Defective Return

Here’s a detailed, step-by-step guide to help you rectify the errors:

- Log in to the Income Tax e-Filing Portal

- Access the Portal: Visit the Income Tax e-Filing website and log in using your PAN, password.

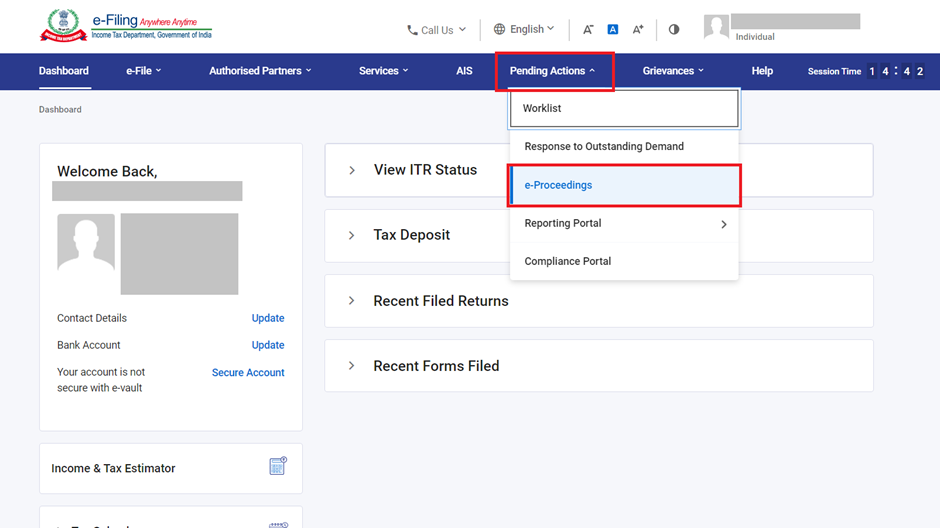

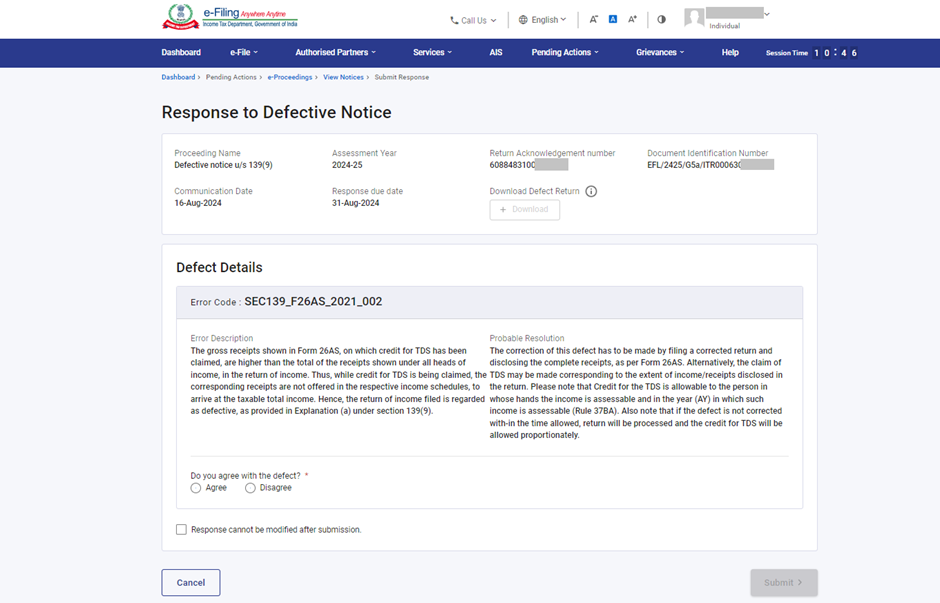

- Click on ‘Pending Actions’, select ‘e-Proceedings’ from the dropdown as shown below.

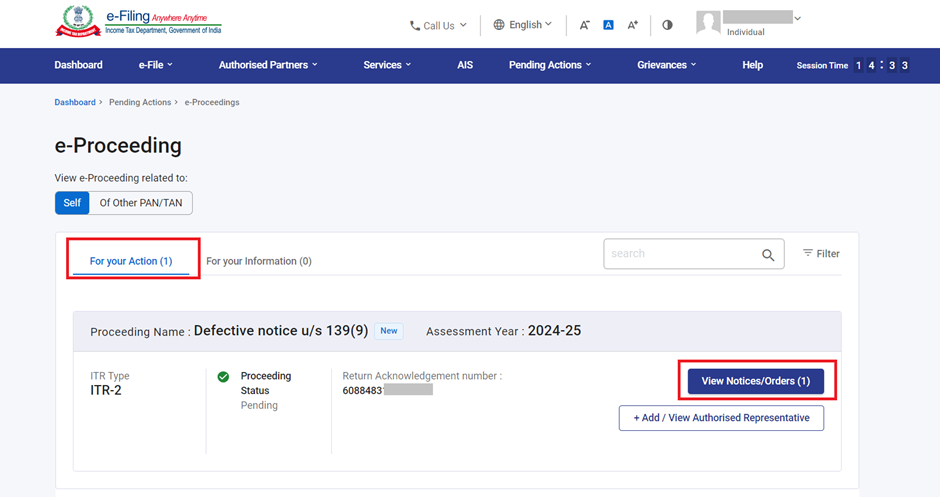

- Click on ‘For your Action’ and find the notice issued under Section 139(9) and click on ‘View Notices/Orders’ to view the details.

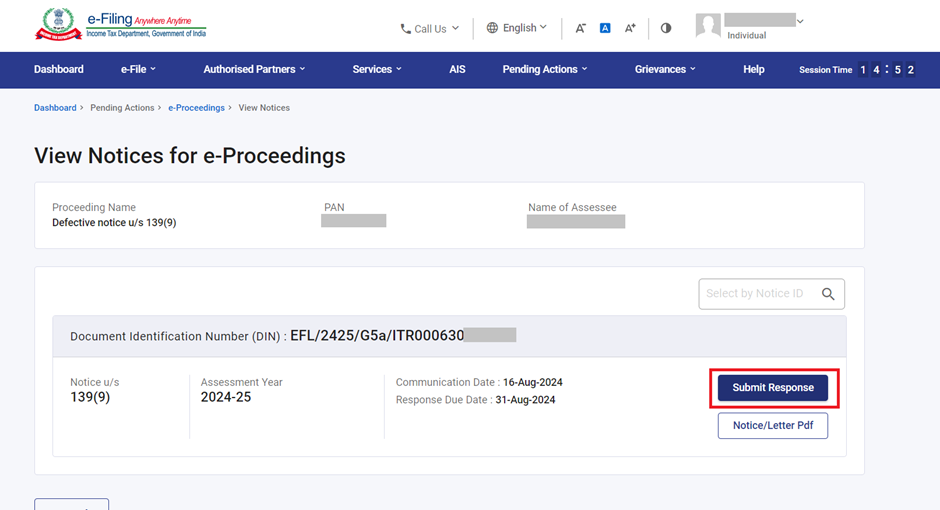

- Click on the ‘Submit Response’ and understand the defects identified. There is not much relevant information under ‘Notice/Letter Pdf’ section.

Read the ‘Error Description’ it will specify the exact errors in your return. Take note of each defect.

- Gather Necessary Documents

- Collect All Supporting Documents: Depending on the defect, gather documents such as TDS certificates, Form 16, Form 26AS, and proofs for deductions claimed.

- Cross-Check Details: Verify that the information in these documents matches the details in your original return.

- Rectify the Errors in Your Return

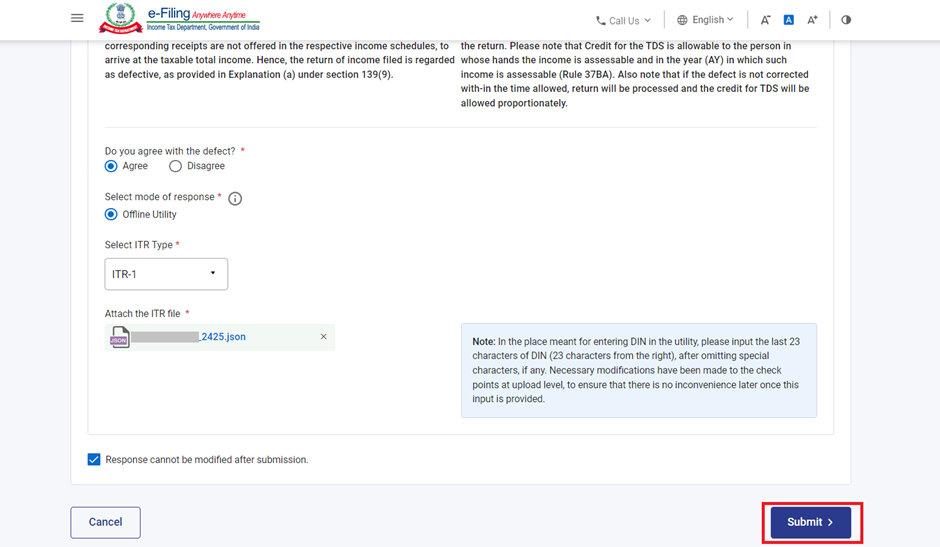

- Correct the Mistakes: Log in to the e-filing portal, go to the offline excel utility and make necessary corrections in the ITR form. Ensure that all fields are accurately filled and generate the Json file.

- Click on ‘Agree’ << Select ‘Offline Utility’ << Select ‘ITR Type’ from the dropdown << Upload the corrected ‘Json file’ << Click on ‘Response cannot be modified after submission’ and finally click on ‘Submit’.

What If You Miss the Deadline?

If you fail to rectify the defects within 15 days, the return may be treated as invalid, resulting in:

- Loss of carry-forward losses

- Ineligibility for refunds

- Interest and penalties on unpaid tax

- Potential legal consequences

Processing Time After Correction:

After you submit the corrected return, the Income Tax Department typically takes 2-4 weeks to process it. During this time, monitor the status of your return on the e-filing portal to ensure everything is proceeding smoothly. Choose us for the ITR filing services.

To avoid future defective return notices:

- Double-Check Before Submission: Always verify your income details, deductions, and TDS before filing.

- Maintain Updated Records: Keep all tax-related documents organized and up-to-date throughout the year.

- Regularly Review Form 26AS: Periodically check Form 26AS to ensure all your income and TDS are accurately reflected.

Ensure Your Returns Are Error-Free

Dealing with defective returns can be daunting, but it doesn’t have to be. At Findtax, we specialize in providing comprehensive tax filing services that ensure accuracy and compliance, saving you time and stress.

Don’t wait for a notice—consult with our experts today to ensure your returns are flawless and your finances secure.

FAQs

- How will I receive notice u/s 139(9)?

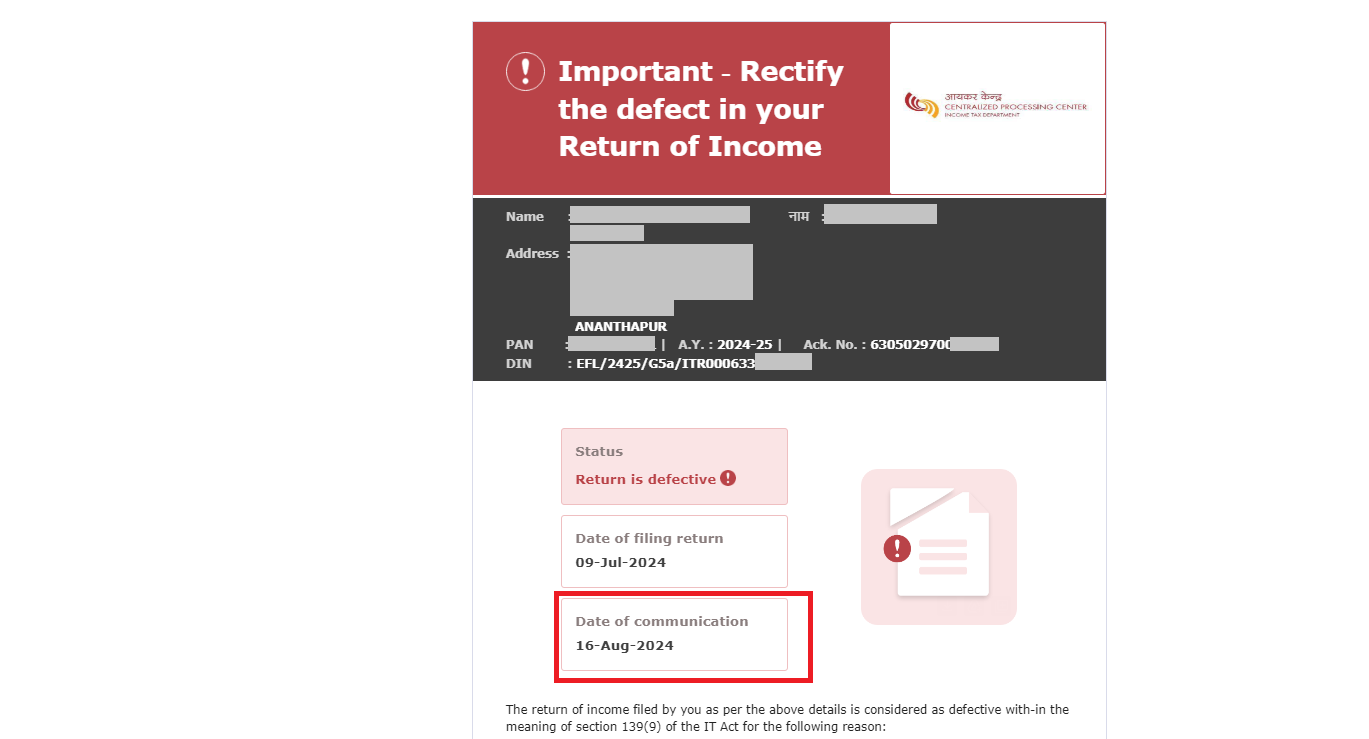

You will receive notice u/s 139(9) from the income tax department on the email ID entered while filing your ITR. Usually, these notices are received from CPC intimations@cpc.incometax.gov.in, and the subject line is ‘Important – Rectify the defect in your Return of Income’

- Where can I find the error description?

In the defective communication mail you can find the reason for defective notice as shown below.

- What will be the due date for response to Defective notice?

Generally, the time period to respond to defective notice is 15 days. However, you may seek adjournment and request for an extension.

- What if I don’t respond to a Defective Notice?

If you fail to rectify the defects within 15 days, the return may be treated as invalid, resulting in:

- Loss of carry-forward losses

- Ineligibility for refunds

- Interest and penalties on unpaid tax

- Potential legal consequences

- Old Regime cannot be availed

- I have been notified about defective returns u/s 139(9). Can I file the return again as a fresh return for that assessment year?

You can either file a fresh or revised return if the deadline for filing the return for that assessment year hasn’t passed. Alternatively, you can respond to a Notice under Section 139. However, once the deadline has passed, you can no longer file a fresh or revised return, and you must respond to the Notice under Section 139(9). If you don’t respond to the notice, your return will be considered invalid or not filed for that assessment year.